The economic and market outlook of 2024

The global economy is still experiencing the aftershocks of the COVID-19 pandemic and the ensuing policy response.

In 2023, central banks tightened policy severely, hoping their actions would return their economies to normal without causing a sharp recession in the process. We think policymakers will largely achieve their goals in 2024 and 2025, and we will let historians decide whether this was by luck or good judgment. We think labor markets, wage growth and inflation will return to somewhere near normal levels as a period of policy-induced weak growth rebalances labor markets and economies as a whole.

In terms of the outlook for financial markets, we are becoming slightly more optimistic on most asset classes following the bond-led weakness so far in 2023. Bond yields have risen to near two-decade highs and offer the prospect of decent returns for the first time in many years. If we are correct that US economic growth will slow notably to a below-trend (but not recessionary) pace in the near term, then wage growth and inflation should fall further. This could support a modest loosening cycle, although we doubt yields will fall anywhere near the levels witnessed in the past decade.

On the topic of emerging markets, 2024 could be the start of a prolonged period of better equity returns on both an absolute (versus cash) and relative (versus developed world) basis. Valuations are attractive, and GDP and corporate earnings growth should be decent. In addition, the sector is unloved and arguably underinvested. Emerging market (EM) currencies are also attractive, especially versus the US dollar, and EM currency appreciation could provide a modest boost to returns.

Growth

Broadly resilient but regionally divergent

As we move into 2024, we expect the US and other overheated economies to cool as recent supporting factors fade or roll off completely.

Excess US savings and the savings rate are declining. Consumption in 2023 was supported by the use of savings accumulated during the COVID-19 pandemic. Faced with higher cost of living, higher cost of refinancing a mortgage or even a jump in prices for going on a sunny vacation, consumers were able to tap into their excess savings.

Supportive fiscal policy of 2023 is unlikely to persist. We expect the 2024 fiscal deficit to be smaller than 2023, which means fiscal policy will become contractionary, weighing on economic activity.

The services sector is slowing. As we approach the end of 2023, the services sector appears to be losing some steam as the post-pandemic boom for service consumption fades and service prices have become somewhat stretched. We expect that to continue in 2024.

Inflation assistance was a one-off. A rollover in supply-chain constrained goods categories, such as secondhand cars, had a similar effect. Although these assists are powerful, we don’t believe they will repeat in 2024.

As supporting factors fade, the headwinds from aggressive monetary policy actions and tight financial conditions are likely to lead to slower economic activity. Three things stand out:

After one of the most aggressive hiking cycles ever, central banks have brought interest rates firmly into restrictive territory. High interest rates mean it’s far more expensive to get a loan, it’s far more expensive to refinance your mortgage and the interest rate charged on your credit card is far more punitive to your finances. Of course, it takes a while for higher interest rates to have an effect on consumer and business behavior.

For businesses, a lot of the borrowing was done before interest rates started to rise, and high refinancing costs haven’t yet come into play. We think high interest rates will persist, which means people will have to borrow at much higher rates, and companies that refinance debt will have to deal with extra pressures on their profitability. Therefore, the biproduct of higher interest rates will likely be an increase in consumer and corporate delinquencies and defaults.

Banks have tightened their lending standards. Suppose you’re a midsize business and you need a loan to build a new factory. Unlike a few years back, you’re likely to struggle to obtain financing without offering extra guarantees (for example, more collateral). This, alongside higher interest rates, should dampen credit creation in 2024, leading to slower economic activity.

Manufacturing is still contracting; However, the latest survey data suggest that it may have bottomed out, creating a reasonably positive backdrop for 2024.

Inflation

The key drivers behind the latest fall in inflation rates were mostly “acyclical” or supply-side driven. As a result of lower commodity prices (for example, natural gas, oil), falls in certain goods prices (for example, secondhand cars) and resolved supply-chain disruptions (cost of shipping normalized from 10 times above average back to average rates), global headline inflation remains notably above target.

We think 2024 will see demanddriven inflation factors move lower and global inflation rates come closer to central bank targets in the developed world as economic growth slows. Again, three things stand out:

Shelter inflation (mostly relevant in the US) should continue to roll over as official measures catch up with leading private-sector rental inflation measures. Year-on-year shelter CPI took twice as long to reach its peak compared to the actual rents. A similar dynamic is likely to play out as shelter CPI declines.

Cooling labor markets should lead to lower job openings, higher unemployment and slower wage growth. We expect 2024 to see labor markets continuing to cool and wage growth pressures slowly but firmly dissipating.

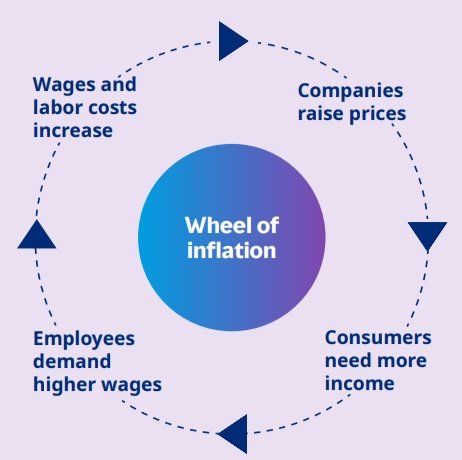

Wheel of inflation. When wage growth is increasing, companies try to pass on that cost to consumers to protect their margins. Consumers, facing higher prices, then go back to their employers and bargain for even higher wages. The higher the inflation expectations, the faster the wheel spins. Central banks try to slow the wheel by hiking interest rates, which normally leads to higher unemployment and reduced wage-growth pressures.

Central banks

Higher for longer (depending on where)

We believe the developed markets central bank hiking cycle is largely over and central banks will keep rates at current levels until they are more certain that inflation will get back to target and stay there. The focus will now shift to whether they can begin cutting rates. We believe three conditions need to be met for this to happen:

Inflation falls closer to target and is seen as likely to stay there.

Growth is weak.

Unemployment rises and wage growth declines.

Key risks

Identified but manageable

As we look at economies in 2024, we see a number of risks bubbling, although, ultimately, we see these as manageable:

1. Geopolitical tensions

Geopolitical events are notoriously hard to predict and tend to be short-lived in financial markets. However, some events can have longer-term effects than others. We are therefore cognizant that escalation in geopolitical tensions can cause significant risks for asset allocators.

2. Elections

Countries representing more than 57% of world GDP9 are hosting elections in 2024; most notably, the US.

3. Financial incidents

The high-profile struggles and failures of US regional banks (including Silicon Valley Bank, Signature Bank, Silvergate Bank and First Republic Bank) remind us that in a high-interest-rate environment, the risk of financial incidents is elevated. As we go through 2024, we expect weak businesses to struggle. The financial system is far more resilient and much less leveraged, while private-sector balance sheets are overall in good shape and policymakers have shown clear willingness to act as the ultimate backstops if things get out of hand.

Markets

2023 market recap

Global government bond yields have risen sharply in 2023, except in China. Nominal bond yields have risen across the entire curve — specifically, on the front end of the curve — as higher interest rates have fed into bond markets, and risk premia have arguably increased as well. In 2023, US twoyear yields rose 0.4% to 4.8% and 10-year yields rose 0.6% to 4.4%, both near cycle highs.

Equity markets have remained resilient but not without volatility. Early in 2023, DM equities rallied as the so-called “Magnificent Seven” technologyrelated stocks drove the market higher. Equities struggled in the second half of 2023 as more hawkish central bank rhetoric soured investor sentiment.

Corporate bond spreads have tightened a little and remain just a touch lower than their long-term average. Growth fixed income assets have generally been quite positive in 2023. Global high yield has been positive as spreads tightened, and all-in yields remained close to the 9% mark. The effects of rising defaults have been muted in 2023 and have not weighed on performance significantly. EM debt, both hard currency and local currency, was positive, with the local-currency segment outperforming. Frontier market debt also performed strongly and was one of the best-performing bond asset classes in 2023.

2024 market outlook

Equities

As we look forward to 2024, we approach the year-end modestly overweight equities. We believe a period of macroeconomic normalization is ahead — with economies returning to trend and wage growth and inflation falling — and that it will be a positive environment for equities.

Growth fixed income

Growth fixed income Positioning for 2024 sees us lean into EM debt and its various subsegments, including frontier market debt (FMD). High yields are available in frontier debt, and we think debt and default worries for the asset class as a whole are overblown.

Defensive fixed income

As we move closer to the end of the cycle, we believe increasing duration is becoming more attractive. As a result, we have moved nominal government bonds to modestly overweight. Nominal yields are attractive, even if they have pulled back from their cycle highs, which means government bonds now offer attractive valuations even with our view that central banks are not close to beginning to cut interest rates.

Currency

Our sentiments on the dollar remain bearish, and we expect it to weaken over time. A high valuation, paired with large twin deficits, leads us to prefer other currencies. A near-term economic growth slowdown in the US is also a headwind. In addition, we continue to favor EM currencies, which generally offer high real yields; EM rate-cutting cycles can also coincide with currency appreciation (the opposite of what often happens in DMs).

Feel free to contact Humble Goode Financial if you have an interest in learning more. We're committed to engaging in discussions about your options and delivering well-balanced advice promptly for a brighter 2024.

General Advice Warning:The information on this website is intended to be general in nature and is not personal financial product advice. It does not take into account your objectives, financial situation or needs. Before acting on any information, you should consider the appropriateness of the information provided and the nature of the relevant financial product having regard to your objectives, financial situation and needs. In particular, you should seek independent financial advice and read the relevant product disclosure statement (PDS) or other offer document prior to making an investment decision in relation to a financial product.